(203) 920-4774

OUR BLOG

Expert Financial Perspectives

April 2020 Newsletter

April 24, 2020

Tax Refund: Spend or Save

About 72% of taxpayers received a refund in 2018 and 2019. Here’s how consumers spent the tax refunds they received in 2018 and what they planned to do with their 2019 refunds.

Social Security May Offer a Lifetime of Protection

Social Security is much more than a retirement program. Most Americans are protected by the Old-Age, Survivors, and Disability Insurance (OASDI) program — the official name of Social Security — from birth through old age. Here are four times in your life when Social Security might matter to you or the people you care about.

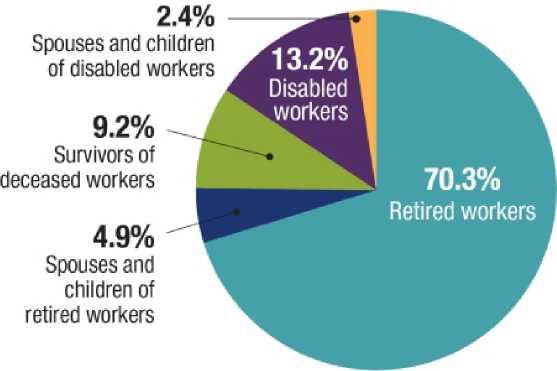

A Wide Safety Net

Current Social Security beneficiaries

Source: Social Security Administration, 2019

When You Start Your Career

Your first experience with Social Security might be noticing that your paycheck is smaller than you expected due to FICA (Federal Insurance Contributions Act) taxes. Most jobs are covered by Social Security, and your employer is required to withhold payroll taxes to help fund Social Security and Medicare.

Although no one likes to pay taxes, when you work and pay FICA taxes, you earn Social Security credits, which enable you (and your eligible family members) to qualify for Social Security retirement, disability, and survivor benefits. Most people need 40 credits (10 years of work) to be eligible for Social Security retirement benefits, but fewer credits may be needed to receive disability benefits or for family members to receive survivor benefits.

If You Become Disabled

Disability can strike anyone at any time. Research shows that one in four of today’s 20-year-olds will become disabled before reaching full retirement age.1

Social Security disability benefits can replace part of your income if you have a severe physical or mental impairment that prevents you from working. Your disability generally must be expected to last at least a year or result in death.

When You Marry…or Divorce

Married couples may be eligible for Social Security benefits based on their own earnings or on a spouse’s earnings.

When you receive or are eligible for retirement or disability benefits, your spouse who is age 62 or older may also be able to receive benefits based on your earnings if you’ve been married at least a year. A younger spouse may be able to receive benefits if he or she is caring for a child under age 16 or disabled before age 22 who is receiving benefits based on your earnings.

If you were to die, your spouse may be eligible for survivor benefits based on your earnings. Regardless of age, your spouse who has not remarried may receive benefits if caring for your child who is under age 16 or disabled before age 22 and entitled to receive benefits based on your earnings. At age 60 or older (50 or older if disabled), your spouse may be able to receive a survivor benefit even if not caring for a child.

If you divorce and your marriage lasted at least 10 years, your former unmarried spouse may be entitled to retirement, disability, or survivor benefits based on your earnings.

When You Welcome a Child

Your child may be eligible for Social Security if you are receiving retirement or disability benefits, and may receive survivor benefits in the event of your death. In fact, according to the Social Security Administration, 98% of children could get benefits if a working parent dies.2 Your child must be unmarried and under age 18 (19 if a full-time student) or age 18 or older with a disability that began before age 22.

In certain cases, grandchildren and stepchildren may also be eligible for benefits based on your earnings.

Know the Rules

To receive any type of Social Security benefit, you must meet specific eligibility requirements, only some of which are covered here. For more information, visit ssa.gov.

1-2) Social Security Administration, 2019

Five Key Benefits of the CARES Act for Individuals and Businesses

By now you know that Congress has passed a $2 trillion relief bill to help keep individuals and businesses afloat during these difficult times. The Coronavirus Aid, Relief, and Economic Security (CARES) Act contains many provisions. Here are five that may benefit you or your business.

- Recovery Rebates

Many Americans will receive a one-time cash payment of $1,200. Each U.S. resident or citizen with an adjusted gross income (AGI) under $75,000 ($112,500 for heads of household and $150,000 for married couples filing a joint return) who is not the dependent of another taxpayer and has a work-eligible Social Security number, may receive the full rebate. Parents may also receive an additional $500 per dependent child under the age of 17.

The $1,200 rebate amount will decrease by $5 for every $100 in excess of the AGI thresholds until it completely phases out. For example, the $1,200 rebate completely phases out at an AGI of $99,000 for an individual taxpayer and the $2,400 rebate phases out at $198,000 for a married couple filing a joint return.

Rebate payments will be based on 2019 income tax returns (2018 if no 2019 return was filed) and will be sent by the IRS via direct deposit or mail. Eligible individuals who receive Social Security benefits but don’t file tax returns will also receive these payments, based on information provided by the Social Security Administration.

The rebate is not taxable. Because the rebate is actually an advance on a refundable tax credit against 2020 taxes, someone who didn’t qualify for the rebate based on 2018 or 2019 income might still receive a full or partial rebate when filing a 2020 tax return.

- Extra Unemployment Benefits

The federal government will provide $600 per week to those who are eligible for unemployment benefits as a result of COVID-19, on top of any state unemployment benefits an individual receives. Unemployed individuals may qualify for this additional benefit for up to four months (through July 31.) The federal government will also fund up to an additional 13 weeks of unemployment benefits for those who have exhausted their state benefits (up to 39 weeks of benefits) through the end of 2020.

The CARES Act also provides assistance to workers who have been affected by the COVID-19 pandemic but who normally wouldn’t be eligible for unemployment benefits, including self-employed individuals, part-time workers, freelancers, independent contractors, and gig workers. Individuals who have to leave work for coronavirus-related reasons are also potentially eligible for benefits.

- Federal Student Loan Deferrals

For all borrowers of federal student loans, payments of principal and interest will be automatically suspended for six months, through September 30, without penalty to the borrower. Federal student loans include Direct Loans (which includes PLUS Loans), as well as Federal Perkins Loans and Federal Family Education Loan (FFEL) Program loans held by the Department of Education. Private student loans are not eligible.

- IRA and Retirement Plan Distributions

Required minimum distributions from IRAs and employer-sponsored retirement plans will not apply for the 2020 calendar year. In addition, the 10% premature distribution penalty tax that would normally apply for distributions made prior to age 59% (unless an exception applied) is waived for coronavirus-related retirement plan distributions of up to $100,000. The tax obligation may be spread over three years, with up to three years to reinvest the money.

The CARES Act provides economic relief for individuals and businesses affected by the coronavirus pandemic

- Help for Businesses

The CARES Act includes several provisions designed to help self-employed individuals and small businesses weather the financial impact of the COVID-19 crisis.

Self-employed individuals and small businesses with fewer than 500 employees may apply for a Paycheck Protection Loan through a Small Business Association (SBA) lender. Businesses may borrow up to 2.5 times their average monthly payroll costs, up to $10 million. This loan may be forgiven if an employer continues paying employees during the eight weeks following the origination of the loan and uses the money for payroll costs (including health benefits), rent or mortgage interest, and utility costs.

Also available are emergency grants of up to $10,000 (that do not need to be repaid if certain conditions are met), SBA disaster loans, and relief for business owners with existing SBA loans.

Businesses of all sizes may qualify for a refundable payroll tax credit of 50% of wages paid to employees during the crisis, up to $10,000 per employee. The credit is applied against the employer’s share of Social Security payroll taxes.

Why You Might Need Disability Income Insurance

Your ability to earn an income may be your most valuable asset. It might be difficult to make ends meet if you are unable to work due to illness or injury.

According to one report, only 34% of men and 20% of women said they felt extremely confident in supporting their households during a period of income loss.1 It’s important to assess your own situation and determine whether you have appropriate financial backup in the event that you cannot work due to a disability.

Your employer may offer long-term disability coverage, but you could lose your subsidized coverage if you change jobs. Even if you remain covered through your job, group plans typically don’t replace as large a percentage of income as an individual plan could, and disability benefits from employer-paid plans are taxable if the premiums were paid by the employer.

An individual disability income policy could help replace a percentage of your income (up to the policy limits) if you’re unable to work as a result of an illness or injury. Depending on the policy, benefits may be paid for a specified number of years or until you reach retirement age. Some policies pay benefits if you cannot work in your current occupation; others might pay only if you cannot work in any type of job. If you pay the premiums yourself, disability benefits are usually free of income tax. And the policy will stay in force regardless of your employment situation as long as the premiums are paid.

Social Security offers some disability protection, but qualifying is difficult. And the monthly benefit you might receive ($1,258, on average) will probably not be enough to replace your lost income.2

Having an individual disability income insurance policy could make the difference between being comfortable and living on the edge.

A complete statement of coverage, including exclusions, exceptions, and limitations, is found only in the policy. It should be noted that carriers have the discretion to raise their rates and remove their products from the marketplace.

- Council for Disability Awareness, 2019

- Social Security Administration, 2020

Round Rock Advisors LLC is a registered investment advisor. Information in this message is for the intended recipients] only. Please visit our website www.RoundRockAdvisors.com for important disclosures.

This newsletter is intended to provide general information. It is not intended to offer or deliver tax, legal, or specific investment advice in any way. For tax or legal advice, please consult a qualified tax professional or legal counsel. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy will be profitable.

Cited content on in this newsletter is based on generally-available information and is believed to be reliable. The Advisor does not guarantee the performance of any investment or the accuracy of the information contained in this newsletter. For information on the Advisor’s services and fees, please refer to the Round Rock’s Form ADV Part 2. The Advisor will provide all prospective clients with a copy of Round Rock’s Form ADV2A and applicable Form ADV 2Bs. Please contact us to request a free copy via .pdf or hardcopy.

Page 4 of 4

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2020

Recent News

Four Strategic Ways to Save for Your Child’s Financial Future

May 29, 2026

The Importance of Personalized Support in Financial Guidance

February 24, 2026

Unlocking Financial Freedom with Round Rock Advisors

November 21, 2025

Why a Personalized Approach Matters in Financial Planning

November 21, 2025

What to Look for in a Financial Planning Partner: Building Trust, Transparency, and Long-Term Vision

August 15, 2025

The Journey to a Rewarding Career as a Private Wealth Advisor

April 30, 2025