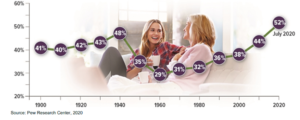

How Long Do Workers Stay with Their Employers?

The median number of years that wage and salary workers had been with their current employer was 4.1 years in January 2020. However, employee tenure tends to vary based on many factors, including the type of occupation, and the impact of the COVID-19 pandemic on tenure remains to be seen.

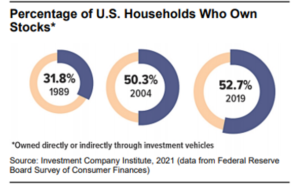

Stock Market Risks in the Spotlight

During March 2021, the widening availability of COVID-19 vaccinations, signs of improving economic conditions, and a third, $1.9 trillion stimulus package brought about more optimistic growth projections. Even though a healthy economy could be good news for many businesses and the financial markets,

rising inflation expectations caused a multi-week sell-off in U.S. government bonds that pushed up longer-term yields and sent the Nasdaq Composite Index into correction territory on March 8, 2021.[1]

Promising a patient approach, the Federal Reserve stated that it would not raise interest rates until the labor market fully recovers and inflation moderately exceeds the 2% target for some time.[2] But some investors worry that sharply higher inflation could force policymakers to boost rates sooner than originally expected.

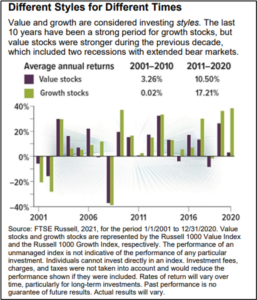

Here’s a closer look at some specific types of investment risk that could influence individual stock prices and/or cause broader market swings during the second half of 2021.

Inflation and Interest-Rate Fears

Inflation and interest rates are two different but closely related investment risks. The Federal Reserve is tasked with fostering full employment and controlling inflation. One way it balances these two goals is by lowering interest rates to stimulate business activity or raising rates to help slow inflation when the economy is heating up too fast.

High inflation erodes the value of investment returns, but when interest rates rise, bond values fall (and vice versa). These risks are obvious considerations for bond owners, but they also impact stocks. When goods, services, and credit cost more, consumers have less purchasing power, which can hurt company earnings and stock prices as well.

Rising bond yields might continue to have a negative effect on stock values, because as they move up, borrowing costs for most businesses also rise, cutting into profits. Higher yields could also entice risk-averse investors to sell their stocks and buy more stable bonds instead.

Legislative or Regulatory Impacts

Some government actions (such as antitrust lawsuits, higher taxes, and more stringent regulations or standards) make it more difficult and expensive for companies to do business, which can adversely affect their earnings and stock prices. On the other hand, government subsidies and tariffs on foreign products can provide competitive advantages.

The Justice Department, Federal Trade Commission, and numerous states are in the midst of antitrust lawsuits or major investigations into the business practices of several market-dominating tech companies.[1] In another example, the Securities and Exchange Commission is considering new standards for corporate disclosures related to environmental, social, and governance risks.[2]

Event or Headline-Driven Volatility

Headline risk refers to the possibility that events reported in the media could hurt a company’s reputation and/or earnings prospects. Troubling news can cause market backlash against a specific company or an entire industry. Companies try to manage this risk through public relations campaigns and other efforts to generate positive news that leaves a good impression on consumers. Events that threaten to disrupt business activity nationwide, regionally, or around the world can cause sudden stock market declines.

The market responds to news, good or bad, almost every day. For this reason, your portfolio should be designed to weather a range of market conditions and have a risk profile that reflects your ability to endure periods of market volatility, both financially and emotionally.

The principal value of bonds may fluctuate with changes in interest rates and market conditions. Bonds redeemed prior to maturity may be worth more or less than their original cost. The return and principal value of stocks fluctuate with changes in market conditions. Shares, when sold, may be worth more or less than their original cost. Investments seeking to achieve higher yields also involve a higher degree of risk

Child Tax Credit for 2021: Will You Get More?

If you have qualifying children under the age of 18, you may be able to claim a child tax credit. (You may also be able to claim a partial credit for certain other dependents who are not qualifying children.) The American Rescue Plan Act of 2021 makes substantial, temporary improvements to the child tax credit for 2021, which may increase the amount you might receive.

Ages of Qualifying Children

The legislation makes 17-year-olds eligible as qualifying children in 2021. Thus, children ages 17 and younger are eligible as qualifying children in 2021.

Increase in Credit Amount

For 2021, the child tax credit amount increases from $2,000 to $3,000 per qualifying child ($3,600 per qualifying child under age 6). The partial credit for other dependents who are not qualifying children remains at $500 per dependent.

Refundable Credit

The aggregate amount of nonrefundable credits allowed is limited to tax liability. With refundable credits, a taxpayer may receive a refund at tax time if they exceed tax liability. For most taxpayers, the child tax credit is fully refundable for 2021. To qualify for a full refund, the taxpayer (or either spouse for joint returns) must generally reside in the United States for more than one-half of the taxable year. Otherwise, under the pre-existing rules, a partial refund of up to $1,400 per qualifying child may be available. The credit for other dependents is not refundable.

Advance Payments

Taxpayers may receive periodic advance payments for up to one-half of the refundable child tax credit during 2021, generally based on 2020 tax returns. The U.S. Treasury will make the payments for periods between July 1 and December 31, 2021. For example, monthly payments could be up to $250 per qualifying child ($300 per qualifying child under age 6).

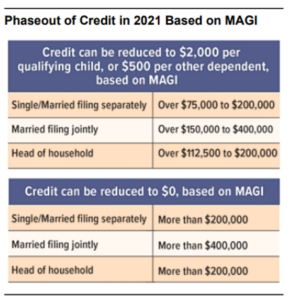

Phaseout of Credit

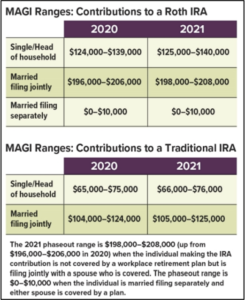

The combined child tax credit (the sum of your child tax credits and credits for other dependents) is subject to phaseout based on modified adjusted gross income (MAGI). Special rules start phasing out the increased portion of the child tax credit in 2021 at much lower thresholds than under pre-existing rules. The credit, as reduced under the special rules for 2021, is then subject to phaseout under the pre-existing phaseout rules.

For 2021, there is no reduction in the credit if the taxpayer’s MAGI does not exceed $75,000 ($150,000 for joint returns and surviving spouses, $112,500 for heads of households). The credit is partially phased out for MAGI exceeding these income limits. At this stage, the credit is reduced by the lowest of the following three amounts:

- $50 for each $1,000 (or fraction thereof) of MAGI exceeding these thresholds

- The total increase in the credit amounts for 2021 [e.g., if 3 qualifying children (2 under the age of 6), then $10,200 increased credit minus $6,000 pre-existing credit = $4,200 increase in credit]

- $6,250 ($12,500 for joint returns, $4,375 for heads of households, $2,500 for surviving spouses); these amounts are equal to 5% of the difference between the higher pre-existing phaseout thresholds and the special thresholds for 2021

The credit cannot be reduced below $2,000 per qualifying child or $500 per other dependent at this stage under this special rule for 2021.

However, the credit can be fully phased out for MAGI in excess of $200,000 ($400,000 for a joint return) under the pre-existing phaseout rules. The credit as reduced in the preceding stage is further reduced by $50 for each $1,000 (or fraction thereof) by which the taxpayer’s MAGI exceeds these thresholds.

Signs of a Scam and How to Resist It

Although scammers often target older people, younger people who encounter scams are more likely to lose money to fraud, perhaps because they have less financial experience. When older people do fall for a scam, however, they tend to have higher losses.[1]

Regardless of your age or financial knowledge, you can be certain that criminals are hatching schemes to separate you from your money — and you should be especially vigilant in cyberspace. In a financial industry study, people who encountered scams through social media or a website were much more likely to engage with the scammer and lose money than those who were contacted by telephone, regular mail, or email.[2]

Here are four common practices that may help you identify a scam and avoid becoming a victim.[3]

Scammers pretend to be from an organization you know. They might claim to be from the IRS, the Social Security Administration, or a well-known agency or business. The IRS will never contact you by phone asking for money, and the Social Security Administration will never call to ask for your Social Security number or threaten your benefits. If you wonder whether a suspicious contact might be legitimate, contact the agency or business through a known number. Never provide personal or financial information in response to an unexpected contact.

Scammers present a problem or a prize. They might say you owe money, there’s a problem with an account, a virus on your computer, an emergency in your family, or that you won money but have to pay a fee to receive it. If you aren’t aware of owing money, you probably don’t. If you didn’t enter a contest, you can’t win a prize — and you wouldn’t have to pay for it if you did. If you are concerned about your account, call the financial institution directly. Computer problems? Contact the appropriate technical

[1] Federal Trade Commission, 2020

[2] FINRA Investor Education Foundation, 2019

[3] Federal Trade Commission, 2020

support. If your “grandchild” or other “relative” calls asking for help, ask questions only the grandchild/relative would know and check with other family members.

Scammers pressure you to act immediately. They might say you will “miss out” on a great opportunity or be “in trouble” if you don’t act now. Disengage immediately if you feel any pressure. A legitimate business will give you time to make a decision.

Scammers tell you to pay in a specific way. They may want you to send money through a wire transfer service or put funds on a gift card. Or they may send you a fake check, tell you to deposit it, and send them money. By the time you discover the check was fake, your money is gone. Never wire money or send a gift card to someone you don’t know — it’s like sending cash. And never pay money to receive money.

For more information, visit consumer.ftc.gov/features/scam-alerts.

Round Rock Advisors LLC is a registered investment advisor. Information in this message is for the intended recipient[s] only. Please visit our website www.RoundRockAdvisors.com for important disclosures.

This newsletter is intended to provide general information. It is not intended to offer or deliver tax, legal, or specific investment advice in any way. For tax or legal advice, please consult a qualified tax professional or legal counsel. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy will be profitable.

Cited content on in this newsletter is based on generally-available information and is believed to be reliable. The Advisor does not guarantee the performance of any investment or the accuracy of the information contained in this newsletter. For information on the Advisor’s services and fees, please refer to the Round Rock’s Form ADV Part 2. The Advisor will provide all prospective clients with a copy of Round Rock’s Form ADV2A and applicable Form ADV 2Bs. Please contact us to request a free copy via .pdf or hardcopy.